L’économie de la participation aux paiements par paliers

AVERTISSEMENT : Les articles reflètent les intérêts et les opinions de leur auteur et ne sauraient constituer des déclarations ou des prises de position officielles de Paiements Canada.

Résumé

Cet article résume les principaux facteurs qui donnent lieu à des relations par paliers dans les systèmes de paiements et d’autres infrastructures de marchés financiers. Plus particulièrement, y sont soulignées les principales considérations entourant l’évaluation quantitative, la surveillance et la résolution des structures par paliers dans un système de paiements modernisé. On voit surtout celles qui ne sont pas assez définies par le 19e des Principes pour les infrastructures de marchés financiers (PIMF). L’absence d’une approche systématique dans la compréhension de l’étagement des arrangements pourrait exposer les organismes de compensation et de règlement des paiements à des risques et compromettre les objectifs d’amélioration et de modernisation des systèmes de paiements. Le texte présente les principaux points qu’il faut considérer pour orienter la compréhension des liens de dépendance dans les ententes de participation par paliers et des risques connexes. Il suggère que des travaux plus poussés aideraient à quantifier et à évaluer les risques de la participation par paliers.

La suite de cet article est en anglais seulement.

Overview1

Modern financial systems exhibit a high degree of interdependence, with connections between financial institutions stemming from both the asset and the liability sides of their balance sheets. These interdependencies within the financial system can be represented as financial networks – broadly understood as a collection of nodes (financial institutions) and links (transactions/payment obligations) between. The level of tiering in such a network sheds light on the structure and flow of these interdependencies and the extent to which certain groups of institutions are dependent on or connected to others. In essence, can a bank A transact directly with a bank D or is bank A’s only means of transacting with bank D by employing a bank B as its clearing agent? Similarly can bank D transact directly with bank B or would it need to go through a bank C which can interact directly with B? Tiering measures this set of network connections. This raises questions of systemic problems such as what happens if either bank B or C fail or how does the failure of banks A or D impact the viability of banks B or C? This is what tiering risk attempts to determine from the perspective of the myriad of risks that arise (e.g. settlement risk, operational risk, liquidity risk, credit risk, contagion, etc.). This piece provides a summary of the key factors that drive the emergence of tiered relationships in payment systems and other financial market infrastructures. More precisely, discussed below are a number of considerations that arise from Principle 19 of the Principles for Financial Market Infrastructures (PFMIs) issued by the Bank for International Settlements (BIS) and the International Organization of Securities Commissions (IOSCO).

Under Principle 19 of PFMIs issued by the BIS and the IOSCO, an “FMI should identify, monitor, and manage the material risks to the FMI arising from tiered participation arrangements”. This Principle specifically speaks to three Key Considerations:

- Definition and Specification: An FMI should identify material dependencies between direct and indirect participants that might affect the FMI;

- Measurement and Threshold Setting: An FMI should identify indirect participants responsible for a significant proportion of transactions processed by the FMI and indirect participants whose transaction volumes or values are large relative to the capacity of the direct participants through which they access the FMI in order to manage the risks arising from these transactions; and,

- Compliance Monitoring and Resolution: An FMI should regularly review risks arising from tiered participation arrangements and should take mitigating action when appropriate.

Principle 19, though prescriptive on what FMIs should, at a minimum, be capable of monitoring, and encouraging direct participation as listed in Section 3.19.11 of the PFMIs’ explanatory notes, leaves a number of central questions at the discretion of the FMI. These central questions specifically relate to the following:

- What types of risk (e.g. credit, liquidity, settlement, systemic, etc.) FMIs should identify as arising from tiered participation?

- What if any interconnections exist between the risks?

- How and what thresholds or other evaluation mechanisms for tiered participation risk, once identified, are to be established for the purposes of monitoring and resolution planning?

- What is meant by FMIs understanding the material dependencies in tiered participation arrangements?

A review of Principle 19 from the vantage point of these considerations and questions illustrates that, the Principle is neither clear as to the key considerations nor how FMIs should address the central questions as they pertain to a modernized payment system. Indeed Principle 19 leaves the definitions, specifications, and identification of the tiering risks it purports FMIs be, at a minimum, able measure and monitor open. It accordingly, falls on the FMI to devise an implantation strategy that best aligns with its constituent market place(s); for Payments Canada, these are presently LVTS and ACSS and at target state, Lynx, SOE, and RTR (hereafter, the Systems).2

This piece argues that in order to adequately assess tiering risk, specify thresholds for monitoring, and subsequent compliance and resolution, a systematic approach is required to understand the emergence of tiering relationships in the Systems Payments Canada operates. Moreover, while Principle 19 has been implemented by signatory jurisdictions, with the exception of Australia, Colombia, and the United Kingdom, very few of these jurisdictions have concretely articulated a systematic understanding of their interpretation of Principle 19 or the thresholds they apply. In the case of Australia, full access to clearing and settlement was granted by default and the market is left to generate tiered relationships as required, however there is limited documentation as to the methodology underpinning their tiering thresholds. It is proposed that not basing policy formulation and compliance on such a systematic understanding of the emergence of tiering arrangements as they pertain to the Systems could expose Payments Canada to risks the PFMIs seek to mitigate and compromise the public policy objectives that underlie modernized payment systems.

For the sake of clarity, especially with this piece using the terms “direct participant” and “clearing agent”, it is helpful to define these terms at the outset. The piece uses the term direct participant to mean any financial or other institution that conducts clearing and settlement directly in the financial market infrastructure. By contrast, a clearing agent is a direct participant that is registered on the FMI as processing transactions on behalf of other institutions not directly participating in the FMI. In this case a clearing agent is a direct participant, but a direct participant need not be a clearing agent.

Economic Dynamics of Tiered Participation

Whilst regulatory considerations under the PFMIs may at first glance appear to be a simple value and volume accounting exercise, such a simplistic reading of Principle 19 ignores the underlying complexities the Principle expects FMIs to understand. Moreover, with Section 3.19.11 of the explanatory notes of the PFMIs explicitly “encouraging direct participation” upon breach of tiering thresholds, thus indicating a preference for de-tiering, it is important for FMIs to possess a concrete understanding of the implications of de-tiering. Conventional wisdom that de-tiering avoids concentration risk, avoids excess credit and/or liquidity risk between direct and indirect clearers, etc., remains an open empirical question and overlooks broader systemic risk implications that are not obvious at face value. For example, can de-tiering give rise to greater liquidity and solvency strains on other indirect participants under a given direct participant once the liquidity the de-tiered indirect participant has is removed from the direct participant?

Indeed, there exist trade-offs between the risks Principle 19 tries to mitigate with respect to the value and volume of transactions direct participants process on behalf of indirect participants. These trade-offs imply that, incorrectly assessing the risks as part of resolution and thereby forcing a de-tiering event may, rather than protect the direct participant from liquidity risk, actually put liquidity pressures on the direct participant. Imagine for example that a given indirect is systemically important to the internal liquidity management of the direct participant to the tune of accounting for 80% of all flows between the clearing agents indirect participant clients, forcing this indirect to become a direct participant as a result of the 20% of external liquidity flows will potentially have wider implications. In periods of economic stress, this may limit the direct participant’s ability to meet its obligations in a timely manner and potentially generate settlement risk and delays in the Systems. As such, at a systemic level, there are clear and important risk and efficiency issues that are not overlooked by the PFMIs, but need to be considered in any holistic evaluation of what is an appropriate level of tiering in modernized clearing and settlement systems. Policy drafting and monitoring should be cognisant of these broader systemic risks or trade-offs and identify appropriate resolutions which may or may not entail de-tiering.

To better understand the emerging risks of tiered participation in Canada’s modernized payment systems, it should be noted that tiering in payment systems arises from three sources; namely regulation, operational costs, and market dynamics, which are discussed in more detail below.

- Regulation

Regulatory requirements, risk models, and rules guiding access and throughput have the potential to impose prohibitive costs and barriers to direct participation3. For example, Liquidity Costs arising from central bank rules on collateral eligibility and the applicable credit risk models may prohibit certain indirect participants from becoming direct participants. Consequently, the level of direct participation is affected by the central bank’s risk appetite and its willingness to grant a financial institution access to a settlement account and liquidity facility. In addition to this, the Systems’ Access Criteria will also drive tiering. Currently the ACSS has a 0.5% national volume rule as its proxy for risk-based access criterion.4 This and similar rules may reduce the potential for direct participant defaults, in part due to there being fewer and larger direct participants, but also give rise to a paradox of generating tiered relationships but limiting the extent of tiering risk since the likelihood of any individual indirect participant processing material value and volume through its clearing agent diminishes.5 Again in the setting of the Systems’ rules we observe trade-offs between the tiering risks Principle 19 seeks to address.

- Operational costs

Set-up and Running Costs associated with rolling out the technology, infrastructure, and human capital to operate across the various payment streams, testing, maintenance and systems upgrade cycles influence the degree of tiered participation in payment systems. These costs may further prove problematic in the retail system which conflates considerations around exchange and settlement. For example, permitting indirect participants to exchange messages at will forces liquidity constraints on their clearing agents and therefore impinge on the clearing agent’s ability to efficiently manage its intraday liquidity needs. This may in turn lead to clearing agents charging indirect clearers more for settlement services in such a way as to limit access to exchange services provided to indirect clearers by the FMI.

The business model of certain institutions may involve the processing of high value transactions operated by small boutiques. This could include trade support, cash management, and international development to mention a few. Such institutions may periodically have to process large values or volumes of transactions as conditions in the markets they support dictate. For such institutions, it may be operationally difficult, even impractical, from a capital and collateral management perspective to justify the ongoing outlay of maintaining direct participation.

- Market Dynamics

These considerations speak to scale and scope efficiencies that exist in tiered relationships which have systemic implications and benefits to all involved. This is also where the bulk of the complexities exist. Tiered relationships enable:

Liquidity Internalisation and pooling that, allow direct participants to net and offset transactions internally and thereby minimise liquidity outlays at the system level. In other words, when a bank operates as a clearing agent, payments between its clients may be settled on that clearing agent’s own books as “on us” transactions with no liquidity cost implications. Moreover, the ability to pool uncorrelated payments affords a clearing agent increased stability in its liquidity needs and thereby lowers the overall cost of liquidity management.

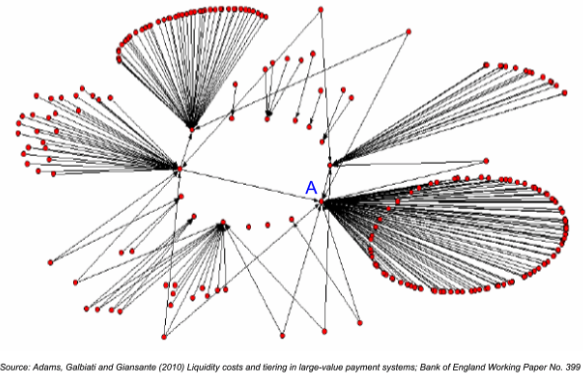

Figure 1: Tiered Participation in the UK’s CHAPS Large Value Payments System

The consequence of this for the FMI is a reduction in multilateral net debit positions that feed into measuring credit risk related exposure at default and also minimising the liquidity risk within the Systems. Therefore, just as an indirect participant processing sizable transactions value or volume through a clearing agent relative to the activity of that clearing agent may result in liquidity strains on the clearing agent as Principle 19 contemplates, where the indirect participant plays an important role in the internal netting of transactions processed by its clearing agent, removing the indirect participant from the tiered relationship can be equally challenging to its clearing agent from a liquidity management perspective. This in turn increases the liquidity risk within the FMI and potentially results in payment bottlenecks regardless of any throughput guidelines or liquidity savings mechanisms in effect.

This trade-off is particularly important where indirect participants employing the clearing services of a particular direct participant reside in a same geographic location and transact frequently with one another. For example, with the majority of Participant Financial Institutions located in Toronto’s M5 postal code, it is reasonable to expect these institutions have strong transaction relationships. Such market localisation may give rise to tiering relationships such as that in the UK’s CHAPS depicted in Figure 1. In such structure, clearing agent “A” under a simplistic reading of Principle 19, may be considered a single point of failure or having too high a percentage of its cleared volumes or value represented by the activities of its indirect clients. However, a more detailed view into the dynamics of these tiered relationships could indicate that the overwhelming majority of this volume or value may be in form of on-us transactions or transactions that smoothen clearing agent A’s liquidity needs and thereby those of the FMI as a whole. In such instances, tiering reflects the systemic importance of client-correspondent relationships and prove liquidity enhancing as opposed to a strain.

Principle 19 further overlooks the pricing of the Trade-off between Market Capture and Risks as captured in different risk-based service offerings direct participants provide to indirect participants. Banks as regulated entities must comply with capital and liquidity regulations, know-your-client (KYC), anti-money laundering (AML), and counter-terrorism financing (CTF) regulations as stipulated by regulators. Moreover, in payment systems, clearing agency arrangements tend to be in a form similar to correspondent banking relationships. Consequently, indirect participants in such systems must maintain deposits or settlement accounts on the books of their clearing agents in order to facilitate transactions (as is the case under ACSS By-law No. 3 and ACSS Rule D3). A mature measure of the risks from tiered participation should account for such arrangements and risk-based service offerings.

Likewise, KYC and routine credit risk management provides the clearing agent insights into the risk profile of the indirect participant for which it processes payments and therefore, the ability to price its service offerings accordingly. A simplistic reading of Principle 19 of the PFMI which only takes into consideration values and volumes processed, overlooks the fundamental risks or lack thereof from such arrangements. For example, if a direct participant requires its clients to maintain cash balances to fully fund transactions, then there is no adverse liquidity pressure put on the direct participant from the clearing and settlement activity it does on behalf of its clients; and this aspect of Principle 19 is therefore moot. Conversely, where the clearing agent provides clients with overdraft or other liquidity facilities, then, the extent to which its clients’ transactions activity places the clearing agent under liquidity strains must be measured against parameters of these liquidity facilities. These parameters include but are not limited to:

- Size of the overdraft or liquidity facility

- The extent to which the liquidity facility is collateralised

- The number of indirect clearers with access to clearing agent provided overdraft facilities

- The frequency and timing of use of the facility

- Duration of negative balances

Concluding Remarks

While Principle 19 of the PFMI rightly requires FMI operators to clearly understand and manage the risks related to tiered participation in their systems, and to take mitigating actions as needed, it is important that operators take a broad view of the many risks posed by tiering arrangements. Specifically, how these risks might interact, as well as any other interdependencies that might naturally emerge in these arrangements. To this end, understanding the material dependencies in tiered participation arrangements requires more than recording the value and volume of transactions undertaken within the payments systems operated by Payments Canada.

Developing a more in-depth toolkit with which to assess the underpinning and emergent network dynamics of FMIs will further strengthen compliance with Principle 19.

Nevertheless, consideration should also be given to putting such metrics in a broader (analytical) context reflecting considerations, questions, and sources of tiered relationships noted above to better understand these decisions, and to better inform Payments Canada interests.

In this respect, the development of benchmark thresholds that reflect the various dependencies and trade-offs in tiered participation arrangements would be a worthwhile endeavour.

Such benchmarks will better inform the undertaking of compliance monitoring, and resolution policy development. This requires a deeper and somewhat more sophisticated thinking around the development of quantitative and qualitative measures of these benchmark thresholds. It would therefore be useful to explore approaches similar to those found in Bank of England research on the impact of de-tiering events in CHAPS and their liquidity implications (e.g. Becher, Milland and Soramäki, 2008; Lasaosa and Tudela, 2008; Adams, Galbiati and Giansante, 2010; Lasaosa and Sunderland, 2013).

The Author

Segun Bewaji

Segun Bewaji

At Payments Canada, Segun has conducted a wide range of research developing quantitative and forecast models that advise Modernization and Payments Canada’s corporate funding model. He has also developed market microstructure models of financial market infrastructures and machine learning within payments. In his role, ‘Segun is the subject matter expert on distributed ledger technology (DLT) and digital/cryptocurrencies, having participated in Project Jasper and ongoing Jasper-Ubin project. He has a strong financial markets background related to supporting over-the-counter (OTC) derivatives origination and trading at HSBC and the Alberta Investment Management Corporation (AIMCo). ‘Segun has a Ph.D. in Computational Finance from the Center for Computational Finance and Economics Agents (University of Essex) specializing in the market microstructure of financial market regulation under the Basel Accords. His research interests include Financial Network Analyses, Agent-based Computational Economics, and computational intelligence in finance and economics.

1 The views presented in this paper are those of the author and do not necessarily reflect the views of Payments Canada.

2 Note that both the SOE and RTR are to be renamed or rebranded in due course.

3 For example, ABC Financial represents an ancillary and small business line of ABC Chain Store Corporation and as such, ABC Financial may not possess the expertise or ability to cheaply and easily acquire the levels of high quality collateral the Bank would require to directly participate in clearing and settlement. Using the services of a direct participant is therefore advantageous.

4 Note that this criterion is a requirement to become a direct participant. However, it does not compel a financial institution to become a direct participant even if that institution does meet the criterion.

5 If an indirect is incapable of meeting the 0.5% rule to warrant direct access under System rules, then it is unlikely to pose any significant risk to its clearing agent. Conversely, an institution that does not satisfy the 0.5% rule may at certain periods in the year (e.g. June and December bond amortization schedules, Equity Index Roll Dates, futures rollover dates, etc.) have its clearing agent process transaction values and volumes significantly in excess of the risk-based access rule.